Legal Loan Agreement Form for the State of California

Legal Loan Agreement Form for the State of California

Free Promissory Note Template New York - It can also detail the process for loan renewal or refinancing.

Loan Agreement Template Florida - The form should include contact information for both parties.

When navigating the complexities of vehicle transactions, having the right documentation is essential, and the Washington Motor Vehicle Bill of Sale form serves as that critical legal instrument. This form captures the necessary details of the sale, including vehicle specifics and the agreed price, ensuring clarity and legality in ownership transfer. For anyone engaged in buying or selling a vehicle in Washington, it's vital to understand this process, and you can find comprehensive resources about these important documents at All Washington Forms.

Promissory Note Texas - A loan agreement is a written contract between a lender and a borrower.

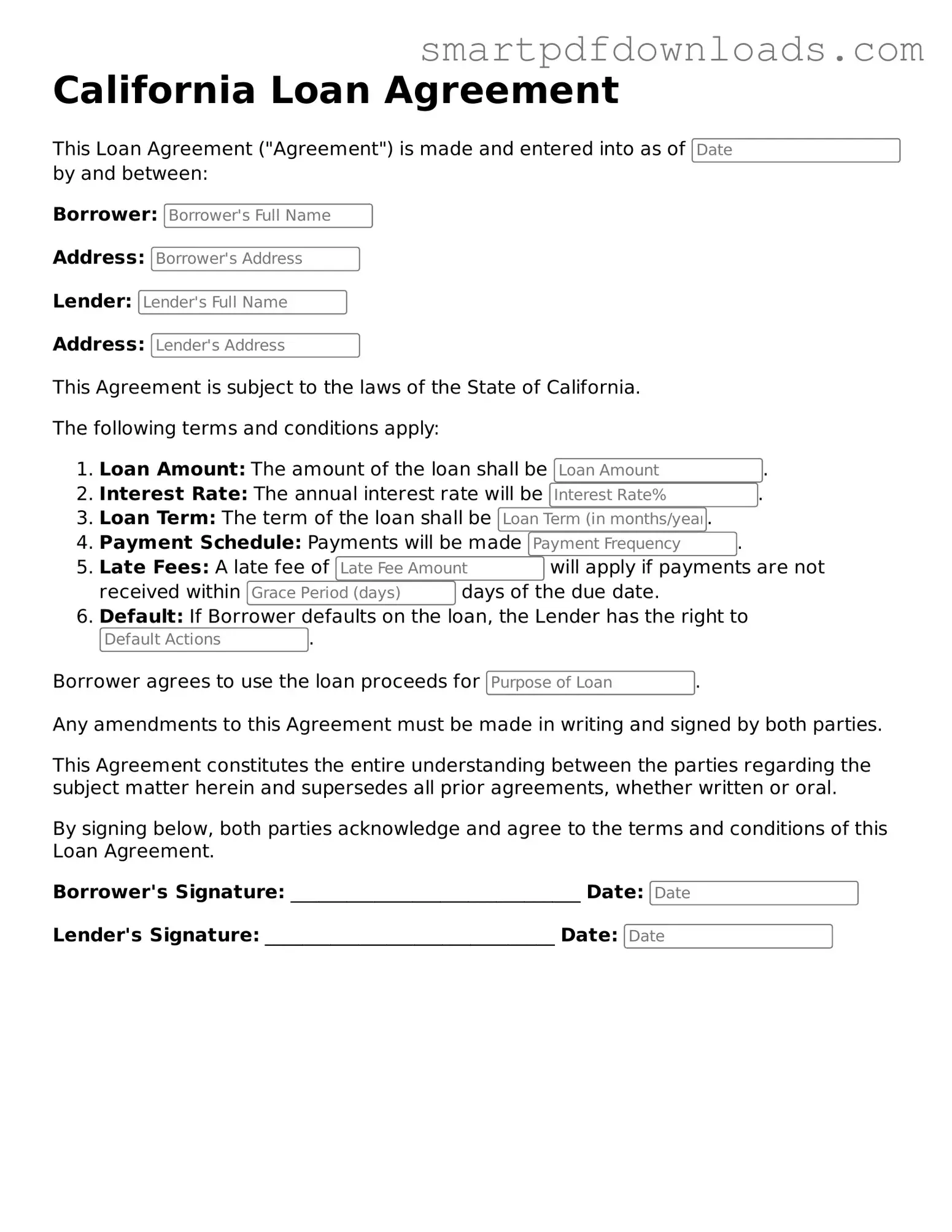

California Loan Agreement

This Loan Agreement ("Agreement") is made and entered into as of by and between:

Borrower:

Address:

Lender:

Address:

This Agreement is subject to the laws of the State of California.

The following terms and conditions apply:

Borrower agrees to use the loan proceeds for .

Any amendments to this Agreement must be made in writing and signed by both parties.

This Agreement constitutes the entire understanding between the parties regarding the subject matter herein and supersedes all prior agreements, whether written or oral.

By signing below, both parties acknowledge and agree to the terms and conditions of this Loan Agreement.

Borrower's Signature: _______________________________ Date:

Lender's Signature: _______________________________ Date:

Completing the California Loan Agreement form requires careful attention to detail. This process involves providing specific information about the loan, the parties involved, and the terms of repayment. Follow these steps to ensure the form is filled out correctly.

Understanding the California Loan Agreement form is essential for both lenders and borrowers. However, several misconceptions can lead to confusion and potential issues. Below are seven common misconceptions about this form, along with clarifications to help you navigate the process more effectively.

Many believe that the Loan Agreement can be used as a one-size-fits-all document. In reality, it should be tailored to fit the specific terms and conditions of each loan. Customization ensures that the agreement reflects the unique circumstances of both parties.

While a signed Loan Agreement is typically enforceable, it must also comply with California law. If the agreement lacks necessary elements or contains illegal terms, it may not hold up in court.

Some individuals think that verbal agreements can modify the terms of a written Loan Agreement. However, California law generally requires that modifications be made in writing to be enforceable.

There are legal limits on interest rates in California. Exceeding these limits can result in penalties, making it crucial to understand the maximum allowable rates before finalizing the agreement.

Although notarization is not always required, certain situations may call for it to enhance the document's validity. Notarization can provide additional proof of authenticity and can be beneficial in disputes.

Borrowers often assume that understanding the agreement is solely the lender's responsibility. However, both parties should fully comprehend the terms to ensure a fair and transparent transaction.

While changing the terms after signing can be challenging, it is not impossible. Both parties can agree to amend the agreement, but this must be documented in writing to be legally enforceable.

A California Loan Agreement is a crucial document for outlining the terms of a loan between a lender and a borrower. However, it is often accompanied by other forms and documents that help clarify the agreement and protect both parties. Below are some common documents used alongside the Loan Agreement.

Understanding these documents can help both lenders and borrowers navigate the loan process more effectively. Each form plays a vital role in ensuring that all parties are on the same page and that their interests are protected.