Legal Promissory Note Form for the State of California

Legal Promissory Note Form for the State of California

Promissory Note Template Florida Pdf - Businesses often rely on promissory notes for cash flow management without refinancing their assets.

Texas Promissory Note Requirements - This form is a vital tool for cash flow management in business transactions.

Completing the New York DTF 84 form correctly is crucial for businesses aiming to qualify as a Qualified Empire Zone Enterprise (QEZE) and secure valuable sales tax exemptions. For detailed guidance on how to navigate this process, it is advisable to visit nypdfforms.com/new-york-dtf-84-form/, which provides comprehensive resources and information related to the application.

Promissory Note for Loan - The note should detail the payment frequency, such as monthly or quarterly payments.

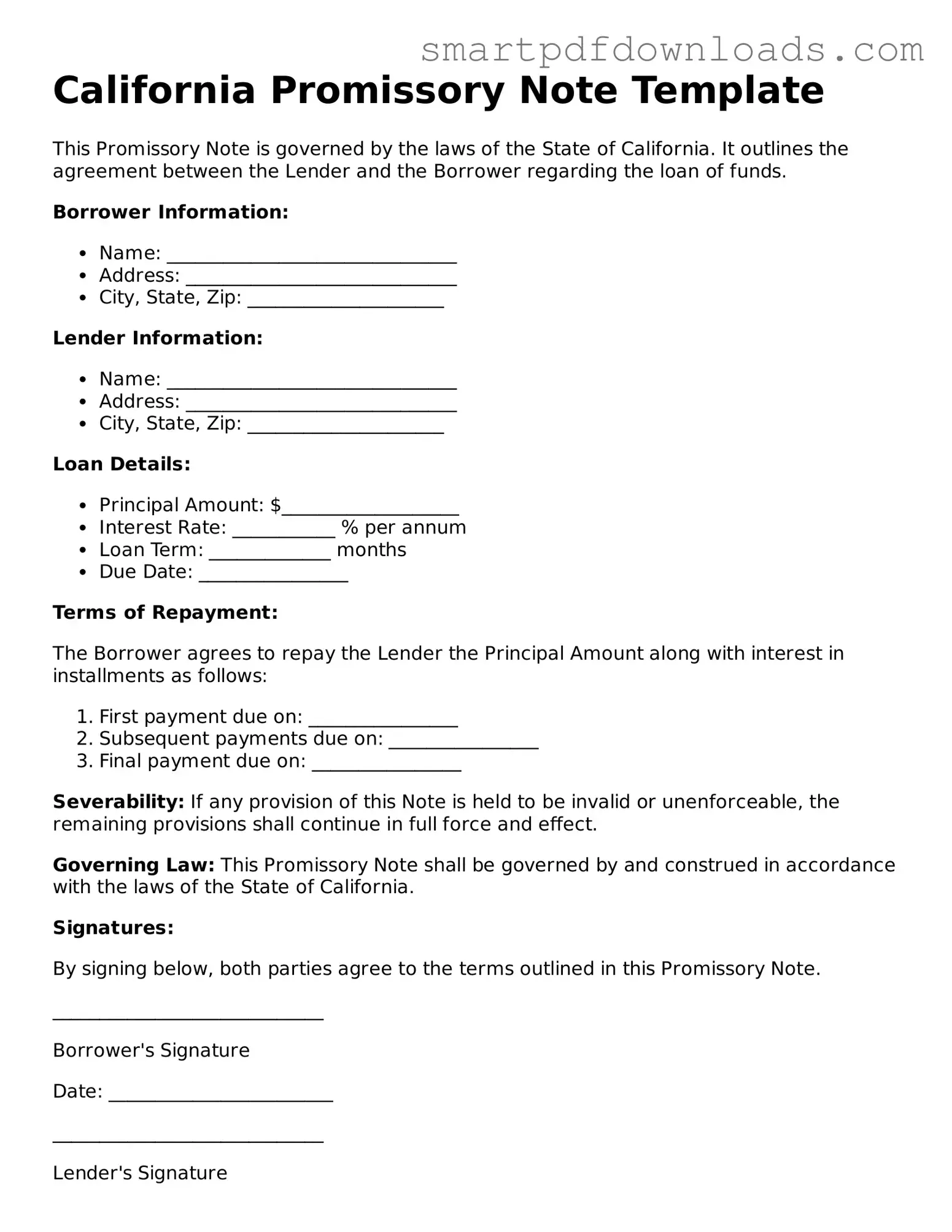

California Promissory Note Template

This Promissory Note is governed by the laws of the State of California. It outlines the agreement between the Lender and the Borrower regarding the loan of funds.

Borrower Information:

Lender Information:

Loan Details:

Terms of Repayment:

The Borrower agrees to repay the Lender the Principal Amount along with interest in installments as follows:

Severability: If any provision of this Note is held to be invalid or unenforceable, the remaining provisions shall continue in full force and effect.

Governing Law: This Promissory Note shall be governed by and construed in accordance with the laws of the State of California.

Signatures:

By signing below, both parties agree to the terms outlined in this Promissory Note.

_____________________________

Borrower's Signature

Date: ________________________

_____________________________

Lender's Signature

Date: ________________________

Once you have the California Promissory Note form in front of you, it’s time to fill it out carefully. This document will outline the terms of the loan agreement between the lender and the borrower. Make sure to have all necessary information ready before you start. Follow these steps to ensure that you complete the form correctly.

After filling out the form, review it carefully to ensure all information is accurate. Both parties should keep a copy of the signed document for their records. This will help in maintaining clear communication regarding the terms of the loan.

Understanding the California Promissory Note form can be challenging, especially with various misconceptions surrounding it. Here’s a breakdown of nine common misunderstandings:

By dispelling these misconceptions, individuals can better navigate the complexities of promissory notes in California, ensuring that their agreements are clear and enforceable.

When dealing with a California Promissory Note, there are several other forms and documents that are often used in conjunction with it. These documents help clarify the terms of the loan and provide additional legal protections for both the lender and the borrower.

These documents play a crucial role in the lending process, ensuring that both parties are protected and that the terms of the loan are clearly defined. Properly preparing and understanding these forms can help prevent disputes and facilitate a smoother transaction.