Free Deed in Lieu of Foreclosure Form

Free Deed in Lieu of Foreclosure Form

Deed of Trust Form - A Deed of Trust secures a loan using real estate as collateral.

The Asurion F-017-08 MEN form serves as an essential tool for users aiming to navigate warranty claims and service requests with Asurion effectively. This form is designed to capture all pertinent information, which not only simplifies the process but also boosts customer assistance. For more details, you can visit https://legalpdfdocs.com/ to ensure a seamless experience.

Title Companies and Transfer on Death Deeds - This deed lets the owner designate beneficiaries to receive property automatically after death.

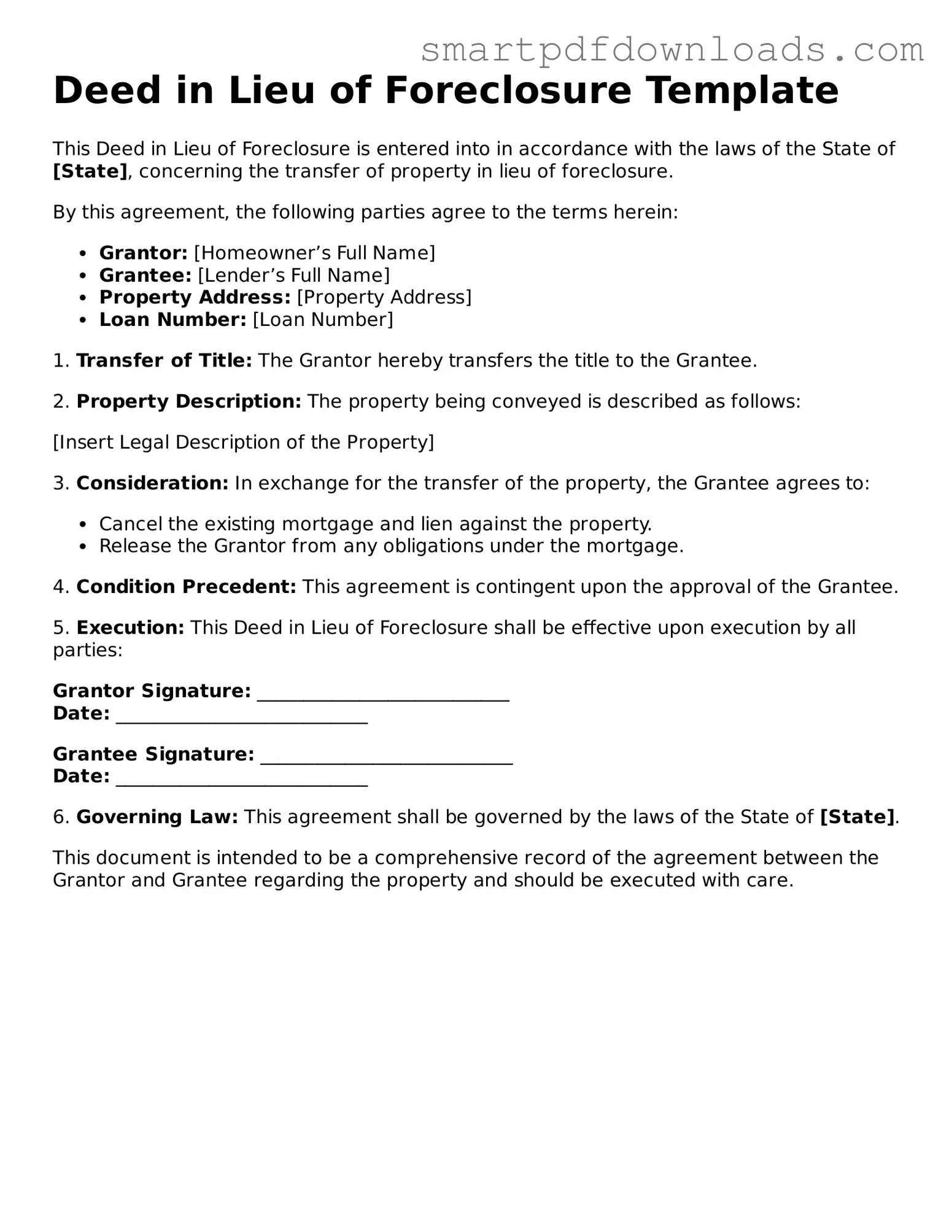

Deed in Lieu of Foreclosure Template

This Deed in Lieu of Foreclosure is entered into in accordance with the laws of the State of [State], concerning the transfer of property in lieu of foreclosure.

By this agreement, the following parties agree to the terms herein:

1. Transfer of Title: The Grantor hereby transfers the title to the Grantee.

2. Property Description: The property being conveyed is described as follows:

[Insert Legal Description of the Property]

3. Consideration: In exchange for the transfer of the property, the Grantee agrees to:

4. Condition Precedent: This agreement is contingent upon the approval of the Grantee.

5. Execution: This Deed in Lieu of Foreclosure shall be effective upon execution by all parties:

Grantor Signature: ___________________________

Date: ___________________________

Grantee Signature: ___________________________

Date: ___________________________

6. Governing Law: This agreement shall be governed by the laws of the State of [State].

This document is intended to be a comprehensive record of the agreement between the Grantor and Grantee regarding the property and should be executed with care.

After completing the Deed in Lieu of Foreclosure form, the next step involves submitting it to the lender. This process may lead to a review period where the lender evaluates the information provided. It’s essential to ensure that all details are accurate and complete to facilitate a smooth transition.

Understanding the Deed in Lieu of Foreclosure can help homeowners make informed decisions during financial difficulties. However, several misconceptions often cloud the reality of this option. Below are ten common misconceptions about the Deed in Lieu of Foreclosure:

By addressing these misconceptions, homeowners can better navigate their options during challenging financial times.

When navigating the complex landscape of real estate transactions, especially during financial difficulties, various forms and documents come into play alongside the Deed in Lieu of Foreclosure. Understanding these documents can help individuals make informed decisions and ensure a smoother process.

Each of these documents plays a vital role in the process surrounding a Deed in Lieu of Foreclosure. By familiarizing yourself with them, you can better navigate the challenges of property ownership and financial distress, ultimately leading to more informed and confident decisions.