Free Deed of Trust Form

Free Deed of Trust Form

Printable Quitclaim Deed - A quitclaim deed can bring clarity to property ownership issues arising in blended families.

A Georgia Quitclaim Deed form is a legal document used to transfer ownership of real estate from one individual to another without making any guarantees about the title's status. This type of deed is often used among family members or in situations where the seller is not concerned about the title's history. For templates and more information, visit legalpdfdocs.com. If you're ready to fill out this form, click the button below.

Deed in Lieu of Foreclosure Meaning - Selling the property may prove beneficial prior to initiating a deed in lieu for some borrowers.

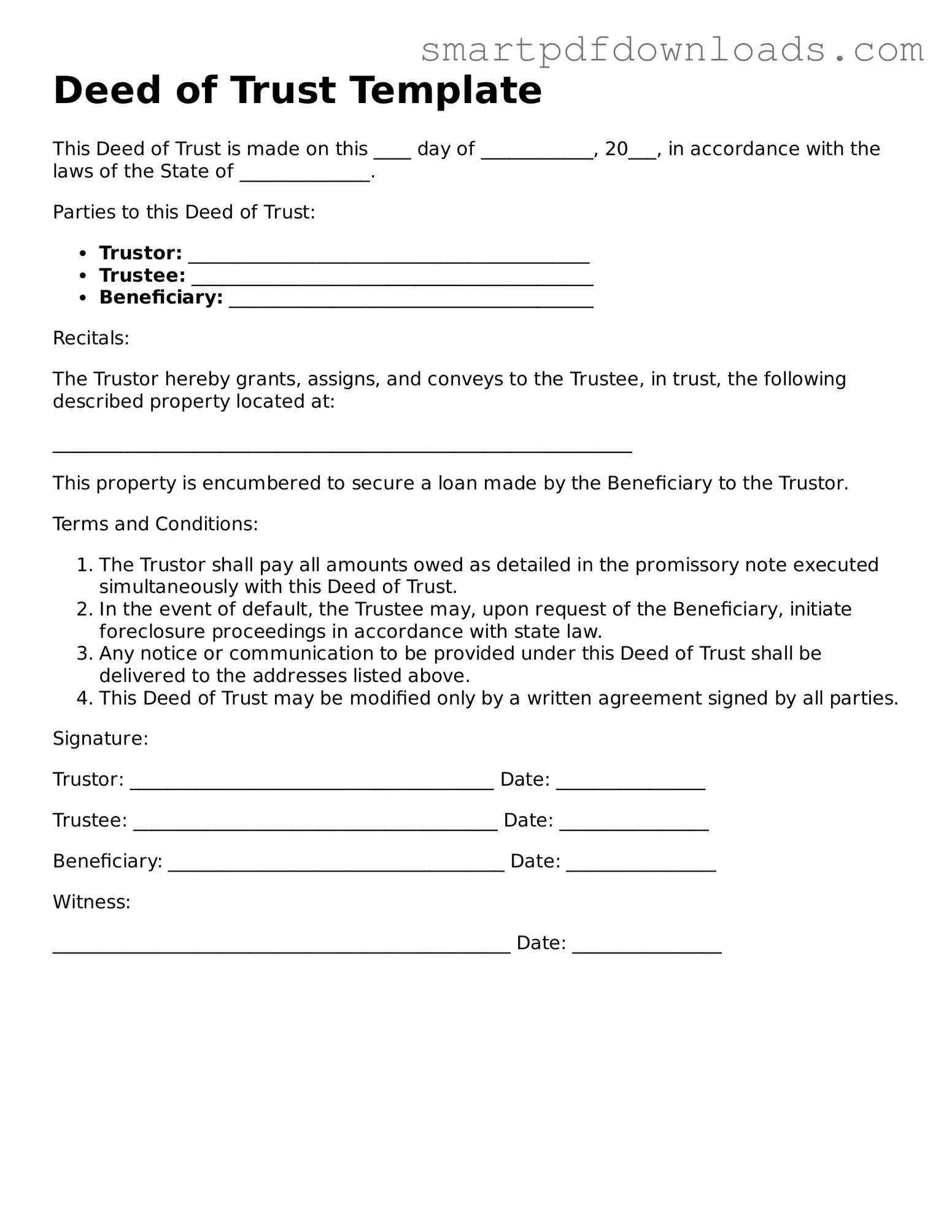

Deed of Trust Template

This Deed of Trust is made on this ____ day of ____________, 20___, in accordance with the laws of the State of ______________.

Parties to this Deed of Trust:

Recitals:

The Trustor hereby grants, assigns, and conveys to the Trustee, in trust, the following described property located at:

______________________________________________________________

This property is encumbered to secure a loan made by the Beneficiary to the Trustor.

Terms and Conditions:

Signature:

Trustor: _______________________________________ Date: ________________

Trustee: _______________________________________ Date: ________________

Beneficiary: ____________________________________ Date: ________________

Witness:

_________________________________________________ Date: ________________

After obtaining the Deed of Trust form, you will need to carefully fill it out to ensure all necessary information is included. This form typically involves details about the borrower, lender, and property. Follow these steps to complete the form accurately.

When it comes to the Deed of Trust, many people hold misconceptions that can lead to confusion and misunderstandings. Here are nine common myths about this important legal document, along with clarifications to help you better understand its purpose and function.

Understanding these misconceptions can help you navigate the complexities of real estate transactions more effectively. Always seek reliable information and consider consulting with a professional when dealing with legal documents.

When dealing with a Deed of Trust, several other forms and documents often accompany it to ensure a comprehensive understanding of the transaction. Each of these documents plays a crucial role in the overall process, providing clarity and legal backing. Below is a list of commonly used documents that you may encounter.

Understanding these documents can greatly aid in navigating the complexities of a real estate transaction. Each one serves a specific purpose, contributing to a smoother process and better protection for all parties involved.