Fl Dr 312 Form

Fl Dr 312 Form

What Happens If Dog Vaccination Is Delayed - Stay informed on when your dog's vaccinations need to be renewed.

To facilitate a smooth ownership transfer, it's essential to use the appropriate forms, such as the legalpdfdocs.com, which provides a template for the Arizona Trailer Bill of Sale, ensuring all necessary information is accurately included for a valid transaction.

Dmv on Veterans - Record-keeping practices are essential for the County Veterans Service Offices involved in processing.

Dd Form 2870 Army Pubs - This form streamlines the process of transitioning medical records between providers.

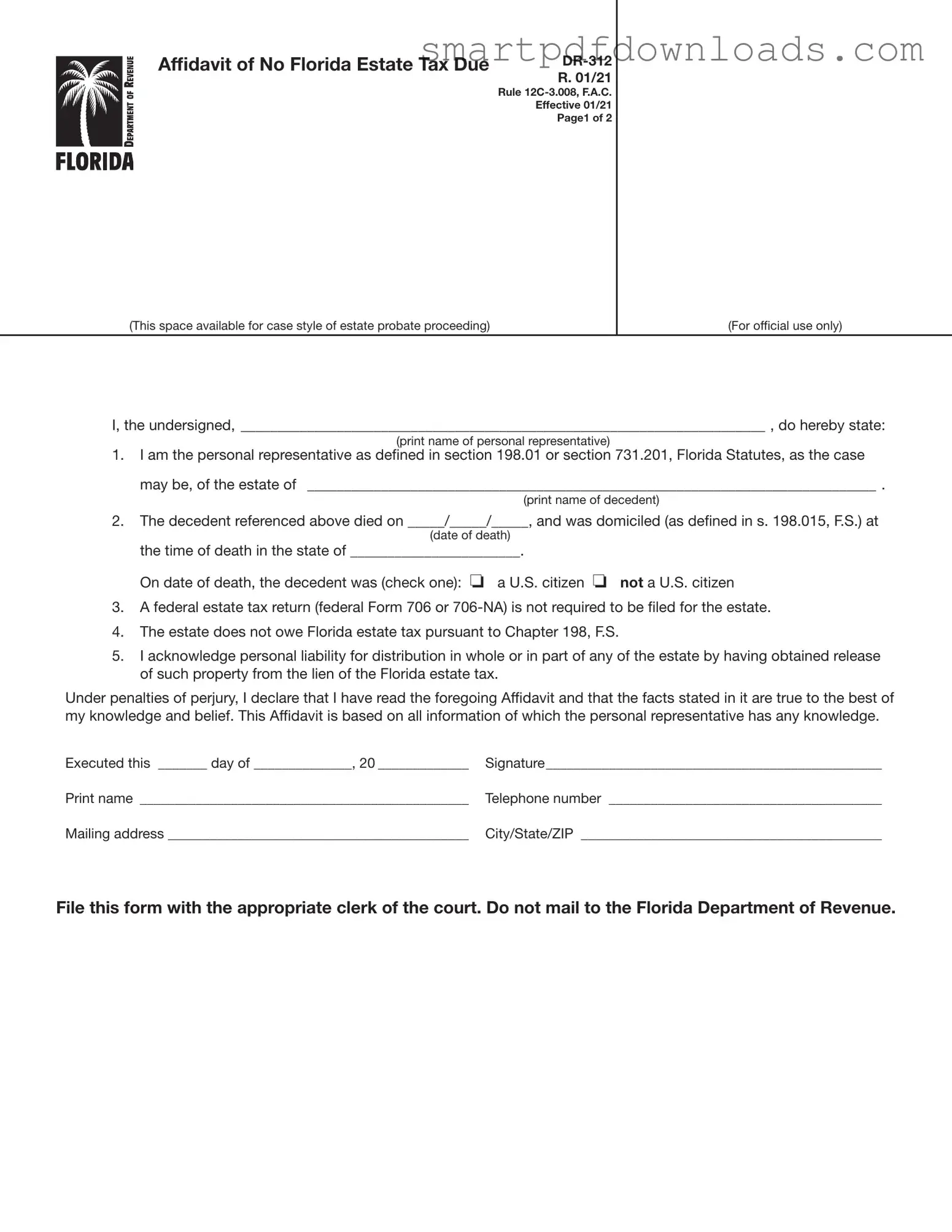

Affidavit of No Florida Estate Tax Due

Rule

Effective 01/21

Page1 of 2

(This space available for case style of estate probate proceeding) |

(For official use only) |

I, the undersigned, _______________________________________________________________________ , do hereby state:

(print name of personal representative)

1.I am the personal representative as defined in section 198.01 or section 731.201, Florida Statutes, as the case may be, of the estate of _____________________________________________________________________________ .

(print name of decedent)

2.The decedent referenced above died on _____/_____/_____, and was domiciled (as defined in s. 198.015, F.S.) at

(date of death)

the time of death in the state of _______________________.

On date of death, the decedent was (check one): o a U.S. citizen o not a U.S. citizen

3.A federal estate tax return (federal Form 706 or

4.The estate does not owe Florida estate tax pursuant to Chapter 198, F.S.

5.I acknowledge personal liability for distribution in whole or in part of any of the estate by having obtained release of such property from the lien of the Florida estate tax.

Under penalties of perjury, I declare that I have read the foregoing Affidavit and that the facts stated in it are true to the best of my knowledge and belief. This Affidavit is based on all information of which the personal representative has any knowledge.

Executed this _______ day of ______________, 20 _____________ |

Signature________________________________________________ |

Print name _______________________________________________ |

Telephone number _______________________________________ |

Mailing address ___________________________________________ |

City/State/ZIP ___________________________________________ |

File this form with the appropriate clerk of the court. Do not mail to the Florida Department of Revenue.

R. 01/21

Page 2 of 2

Instructions for Completing Form

File this form with the appropriate clerk of the court. Do not mail to the Florida Department of Revenue.

General Information

If Florida estate tax is not due and a federal estate tax return (federal Form 706 or

Form

The

Where to File Form

Form

When to Use Form

Form

and a federal estate tax return (federal Form 706 or

Federal thresholds for filing federal Form 706 only: (For informational purposes only. Please confirm with Form 706 instructions.)

Date of Death |

Dollar Threshold |

(year) |

for Filing Form 706 |

|

(value of gross estate) |

|

|

2000 and 2001 |

$675,000 |

|

|

2002 and 2003 |

$1,000,000 |

|

|

2004 and 2005 |

$1,500,000 |

|

|

For 2006 and forward |

|

go to the IRS website at |

|

www.irs.gov to obtain |

|

thresholds. |

|

|

|

For thresholds for filing federal Form

If an administration proceeding is pending for an estate, Form

To Contact Us

Information, forms, and tutorials are available on the Department’s website floridarevenue.com

If you have any questions, or need assistance, call Taxpayer Services at

To find a taxpayer service center near you, go to: floridarevenue.com/taxes/servicecenters

For written replies to tax questions, write to: Taxpayer Services - Mail Stop

5050 W Tennessee St Tallahassee FL

Subscribe to Receive Email Alerts from the Department.

Subscribe to receive an email when Tax Information Publications and proposed rules are posted to the Department’s website. Subscribe today at floridarevenue.com/dor/subscribe.

Reference Material

Rule Chapter

Once you have gathered the necessary information, you can proceed to fill out the Fl DR 312 form. This form is essential for confirming that no Florida estate tax is due for the decedent's estate. Follow these steps carefully to ensure accuracy.

After completing the form, file it with the appropriate clerk of the court in the county where the decedent owned property. Ensure that you do not send this form to the Florida Department of Revenue. This step is crucial to finalize the process and remove any estate tax lien associated with the estate.

Misconception 1: The DR-312 form is only for large estates.

This form can be used for any estate that does not owe Florida estate tax, regardless of its size. It is not limited to large estates.

Misconception 2: Filing the DR-312 form is the same as filing a federal estate tax return.

The DR-312 form is specifically for Florida estate tax purposes. It is not a substitute for the federal estate tax return (Form 706 or 706-NA), which may still be required under certain conditions.

Misconception 3: Only the personal representative can file the DR-312 form.

While the personal representative typically files the form, anyone in actual or constructive possession of the decedent's property can also use it.

Misconception 4: The DR-312 form eliminates all tax liabilities for the estate.

This form only confirms that no Florida estate tax is due. It does not absolve the estate from other potential tax liabilities.

Misconception 5: The DR-312 form must be mailed to the Florida Department of Revenue.

This form should be filed directly with the clerk of the circuit court. Mailing it to the Department of Revenue is not required and can lead to delays.

Misconception 6: Once the DR-312 form is filed, the estate is automatically exempt from all future taxes.

Filing the DR-312 does not guarantee future tax exemptions. If circumstances change, the estate may still incur tax liabilities.

Misconception 7: The DR-312 form can be filed at any time after the decedent's death.

This form should be filed promptly after determining that no Florida estate tax is due. Delays can complicate the estate administration process.

Misconception 8: The DR-312 form is not legally binding.

When signed, the form is a legally binding affidavit. The personal representative acknowledges personal liability for any distributions made based on the information provided.

Misconception 9: You do not need to keep a copy of the DR-312 form after filing.

When dealing with the Fl Dr 312 form, it is often necessary to prepare additional documents to ensure compliance with estate tax regulations. Below is a list of forms and documents that may be used in conjunction with the Fl Dr 312 form. Each document serves a specific purpose in the estate administration process.

Understanding the purpose of each of these documents is essential for the effective administration of an estate. Proper preparation and filing can help avoid delays and ensure compliance with all legal requirements.