Legal Promissory Note Form for the State of Florida

Legal Promissory Note Form for the State of Florida

Promissory Note California - A promissory note can simplify the loan-approval process.

Understanding the importance of a proper transfer of ownership, using the Washington Mobile Home Bill of Sale form can streamline the process and safeguard both the seller and buyer. To facilitate this transaction, it's essential to utilize the correct documentation. For a comprehensive resource, you can refer to All Washington Forms to ensure the sale is completed smoothly and legally recognized.

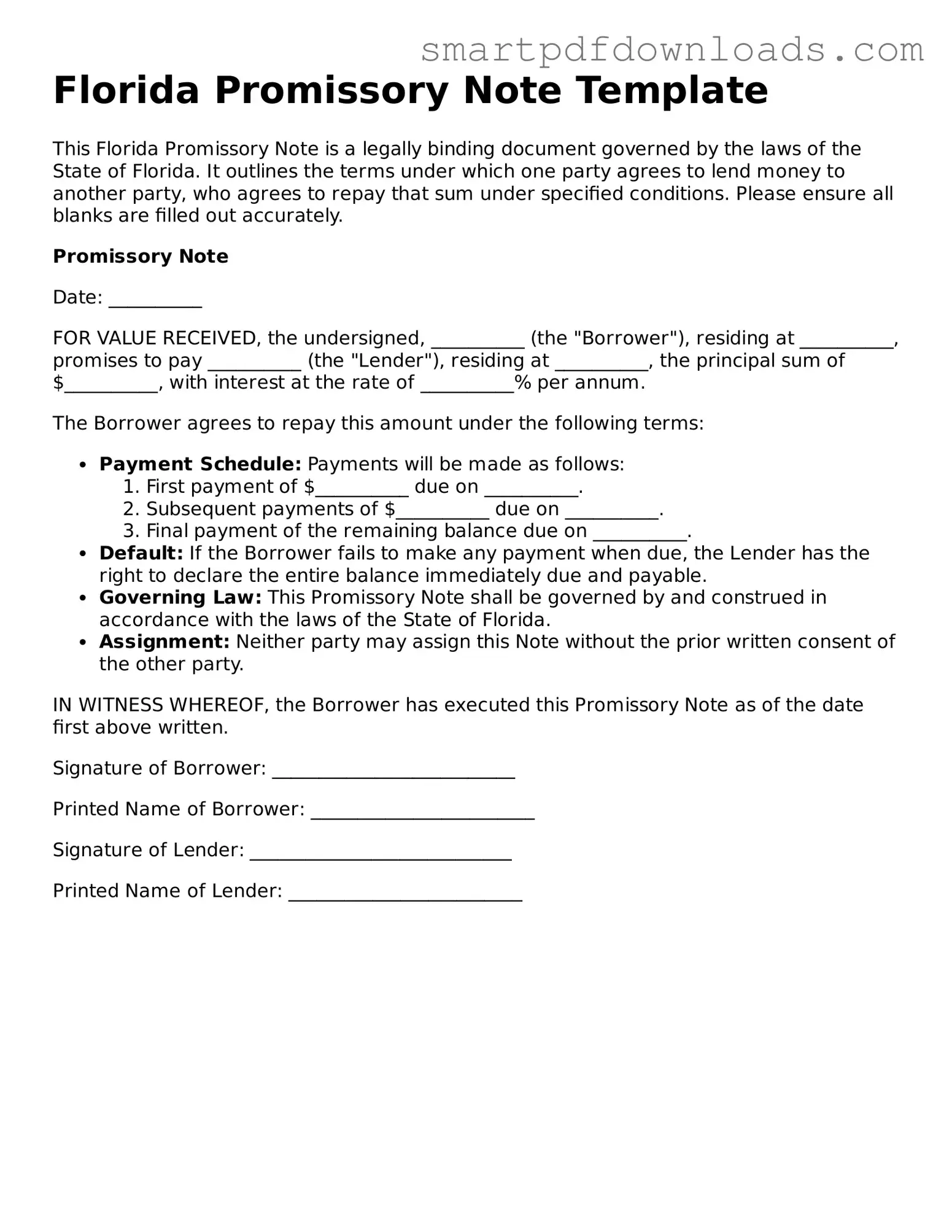

Florida Promissory Note Template

This Florida Promissory Note is a legally binding document governed by the laws of the State of Florida. It outlines the terms under which one party agrees to lend money to another party, who agrees to repay that sum under specified conditions. Please ensure all blanks are filled out accurately.

Promissory Note

Date: __________

FOR VALUE RECEIVED, the undersigned, __________ (the "Borrower"), residing at __________, promises to pay __________ (the "Lender"), residing at __________, the principal sum of $__________, with interest at the rate of __________% per annum.

The Borrower agrees to repay this amount under the following terms:

IN WITNESS WHEREOF, the Borrower has executed this Promissory Note as of the date first above written.

Signature of Borrower: __________________________

Printed Name of Borrower: ________________________

Signature of Lender: ____________________________

Printed Name of Lender: _________________________

After obtaining the Florida Promissory Note form, it’s important to ensure that all necessary information is accurately filled out. This document serves as a written promise to repay a loan under specified terms. Follow these steps to complete the form correctly.

Once the form is filled out, it should be kept in a safe place. Both parties may want to keep a copy for their records. If there are any changes or amendments in the future, those should be documented in writing and signed by both parties as well.

Understanding the Florida Promissory Note form is crucial for anyone involved in lending or borrowing money in the state. However, several misconceptions can lead to confusion. Here are five common misconceptions:

Clarifying these misconceptions can help both lenders and borrowers navigate their financial agreements more effectively.

When dealing with financial agreements in Florida, a Promissory Note is often accompanied by several other important documents. These forms help clarify the terms of the loan and protect the rights of both the lender and the borrower. Below are some commonly used documents that complement the Florida Promissory Note.

Each of these documents plays a vital role in the loan process, ensuring clarity and protection for all parties involved. Understanding these forms can help borrowers navigate their financial commitments with confidence.