Gift Letter Form

Gift Letter Form

Constellation Bracket - Every match is an opportunity for personal and team growth.

Completing the New York DTF 84 form is a critical step for businesses aiming to gain recognition as a Qualified Empire Zone Enterprise (QEZE) and access significant sales tax exemptions. For those seeking guidance on the application process, further information can be found at https://nypdfforms.com/new-york-dtf-84-form, which details the necessary criteria and steps to ensure compliance with requirements set forth by the New York State Department of Taxation and Finance.

How to Buy Melaleuca Without Membership - Address any misunderstandings about the program directly within the feedback section.

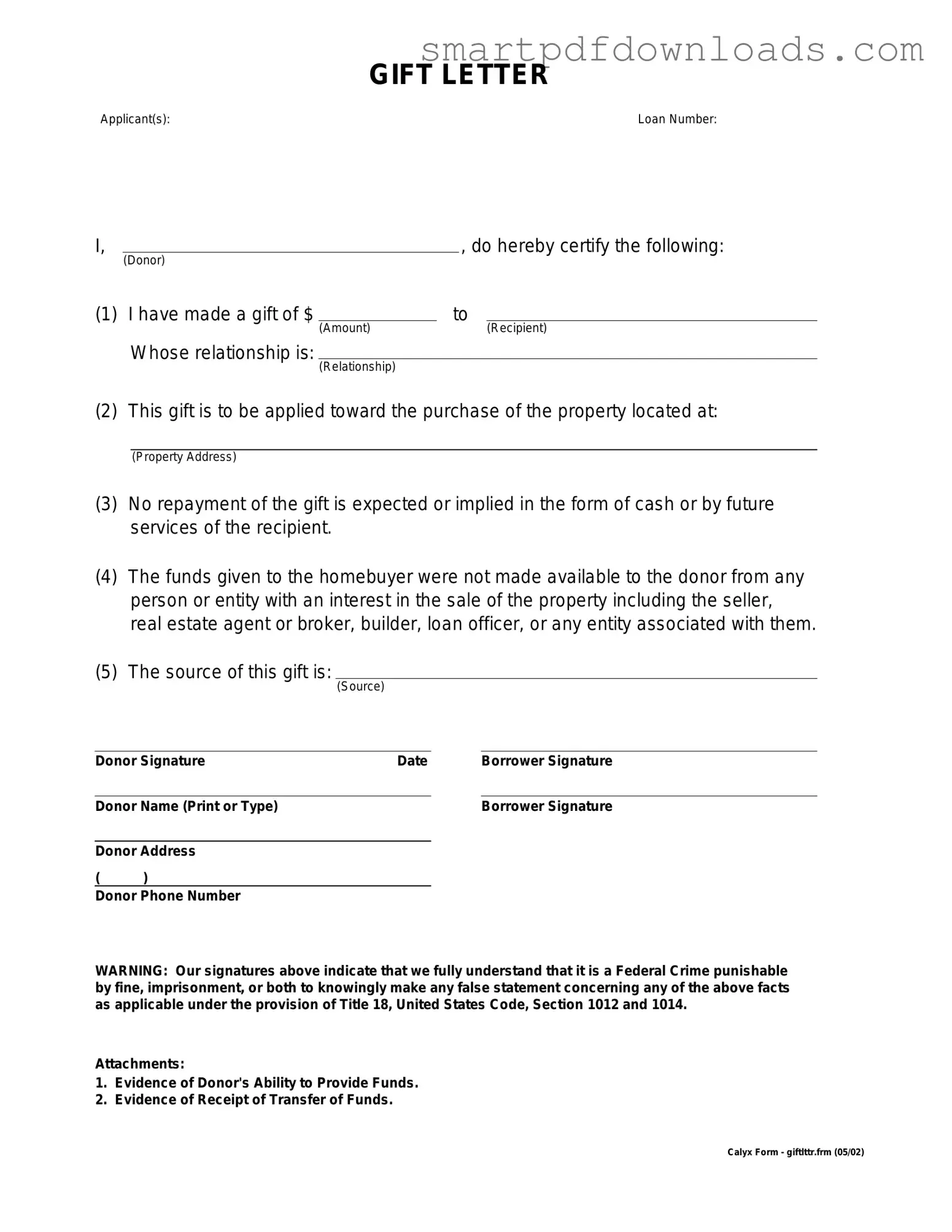

GIFT LETTER

Applicant(s): |

Loan Number: |

I, |

|

|

, do hereby certify the following: |

||

|

(Donor) |

|

|

|

|

(1) I have made a gift of $ |

|

to |

|

||

|

|

(Amount) |

|

|

(Recipient) |

|

Whose relationship is: |

|

|

|

|

|

|

(Relationship) |

|

|

|

(2) This gift is to be applied toward the purchase of the property located at:

(Property Address)

(3)No repayment of the gift is expected or implied in the form of cash or by future services of the recipient.

(4)The funds given to the homebuyer were not made available to the donor from any person or entity with an interest in the sale of the property including the seller, real estate agent or broker, builder, loan officer, or any entity associated with them.

(5)The source of this gift is:

(Source)

Donor Signature |

Date |

Borrower Signature |

||

|

|

|

|

|

Donor Name (Print or Type) |

|

|

Borrower Signature |

|

|

|

|

|

|

Donor Address |

|

|

|

|

( |

) |

|

|

|

Donor Phone Number

WARNING: Our signatures above indicate that we fully understand that it is a Federal Crime punishable by fine, imprisonment, or both to knowingly make any false statement concerning any of the above facts as applicable under the provision of Title 18, United States Code, Section 1012 and 1014.

Attachments:

1.Evidence of Donor's Ability to Provide Funds.

2.Evidence of Receipt of Transfer of Funds.

Calyx Form - giftlttr.frm (05/02)

Once you have the Gift Letter form in front of you, it’s time to fill it out accurately. This form is essential for documenting a financial gift, often required in real estate transactions. Follow these steps carefully to ensure all necessary information is provided correctly.

After completing the Gift Letter form, review it for any errors or omissions. Once everything is in order, submit the form as directed, ensuring that it reaches the appropriate parties involved in the transaction.

Gift letters are often misunderstood, leading to confusion for those looking to use them in financial transactions, particularly in the context of home buying. Here are nine common misconceptions about the Gift Letter form:

Understanding these misconceptions can help clarify the role of gift letters in financial transactions and ensure a smoother process when securing funds for a home purchase.

A Gift Letter form is often used in real estate transactions to document financial gifts from family members or friends to assist with a home purchase. Along with this form, several other documents may be necessary to support the transaction. Here’s a list of related forms and documents commonly utilized in conjunction with the Gift Letter:

Each of these documents plays a crucial role in ensuring a smooth transaction and maintaining transparency between all parties involved. Properly preparing and submitting these forms can significantly enhance the likelihood of a successful home purchase.