Free Loan Agreement Form

Free Loan Agreement Form

Jet Ski Bill of Sale Template - A Jet Ski Bill of Sale can be essential for insurance purposes for the new owner.

The Sample Tax Return Transcript is an important document that provides a summary of key information from a taxpayer's filed return, including income, deductions, and adjustments. For those needing a reference, the Sample Tax Return Transcript form is essential for verifying past tax information, especially when applying for loans or meeting other financial requirements. It is crucial to understand the proper way to fill out this form to ensure accurate reporting and compliance.

Tuberculin Test - The Tuberculosis Skin Test form records the essential details related to TB testing.

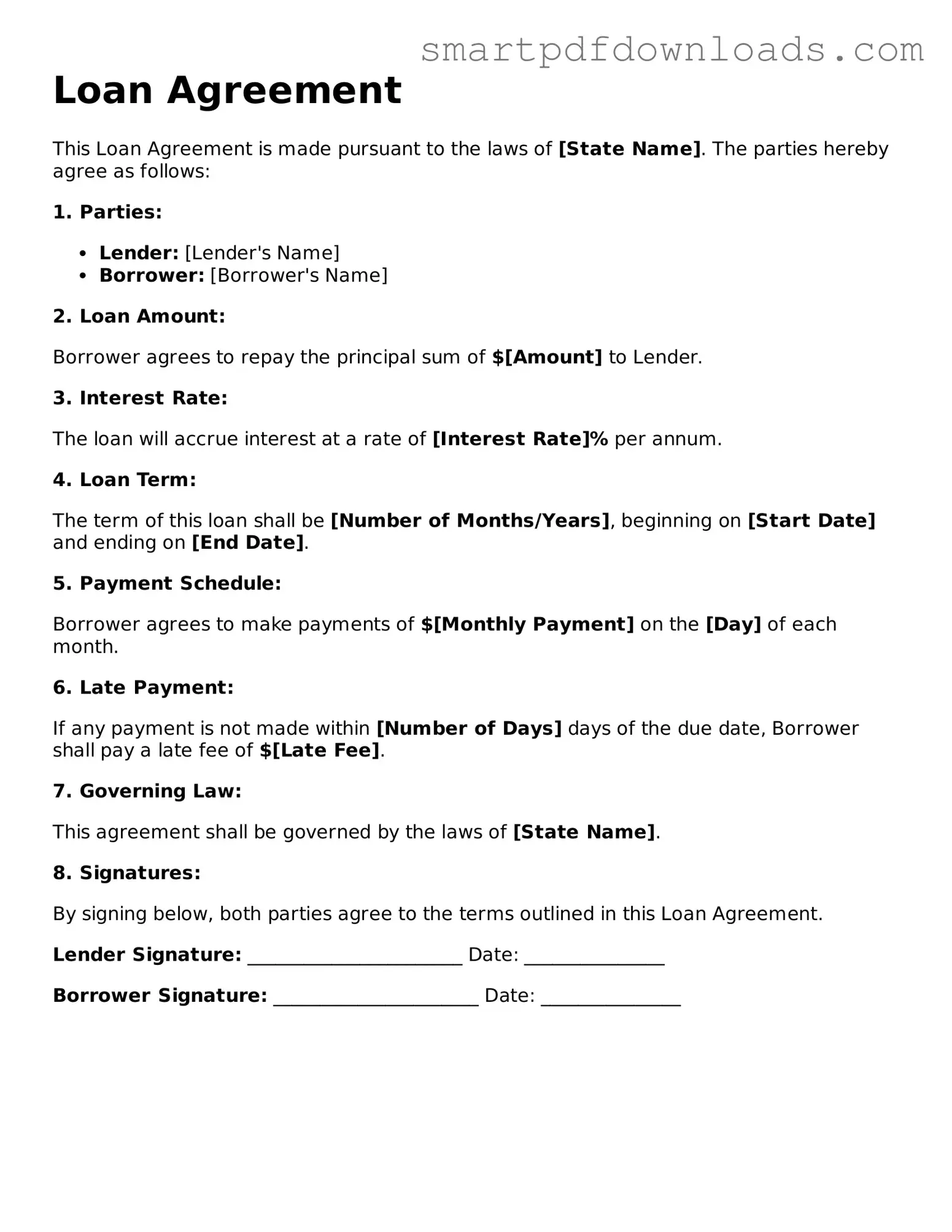

Loan Agreement

This Loan Agreement is made pursuant to the laws of [State Name]. The parties hereby agree as follows:

1. Parties:

2. Loan Amount:

Borrower agrees to repay the principal sum of $[Amount] to Lender.

3. Interest Rate:

The loan will accrue interest at a rate of [Interest Rate]% per annum.

4. Loan Term:

The term of this loan shall be [Number of Months/Years], beginning on [Start Date] and ending on [End Date].

5. Payment Schedule:

Borrower agrees to make payments of $[Monthly Payment] on the [Day] of each month.

6. Late Payment:

If any payment is not made within [Number of Days] days of the due date, Borrower shall pay a late fee of $[Late Fee].

7. Governing Law:

This agreement shall be governed by the laws of [State Name].

8. Signatures:

By signing below, both parties agree to the terms outlined in this Loan Agreement.

Lender Signature: _______________________ Date: _______________

Borrower Signature: ______________________ Date: _______________

Filling out the Loan Agreement form is an important step in securing your loan. Make sure you have all necessary information ready before you start. Follow these steps carefully to ensure the form is completed correctly.

Understanding a Loan Agreement is crucial for both lenders and borrowers. However, several misconceptions can lead to confusion or mismanagement. Here are four common misconceptions about Loan Agreement forms:

Being aware of these misconceptions can help individuals navigate the complexities of Loan Agreements more effectively.

A Loan Agreement is an essential document when borrowing or lending money. However, several other forms and documents often accompany it to ensure clarity and legal protection for all parties involved. Here’s a list of related documents that can be important in the loan process.

Each of these documents plays a crucial role in the loan process, providing clarity and protection for both lenders and borrowers. Understanding them can help ensure a smooth transaction and prevent potential disputes down the line.