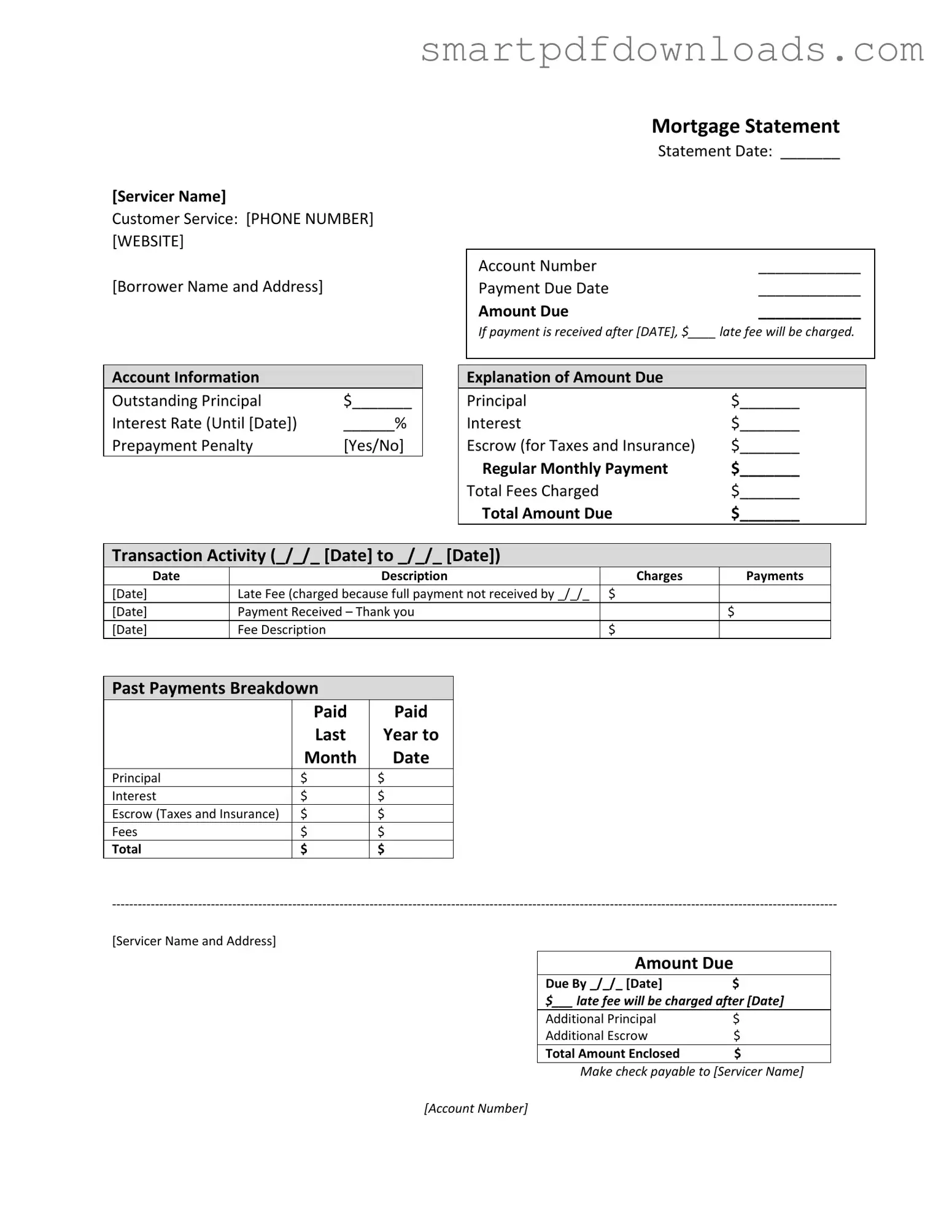

Mortgage Statement Form

Mortgage Statement Form

Wage and Tax Statement - It is important to keep track of any corrections made to the W-2 when filing the W-3.

To effectively manage your financial responsibilities, it is crucial to utilize a Durable Power of Attorney, which allows a trusted individual to act on your behalf, ensuring that your affairs are handled according to your wishes during any period of incapacity.

Navpers 1336 3 - A leave address and telephone number provide necessary contact information for follow-up.

[Servicer Name]

Customer Service: [PHONE NUMBER] [WEBSITE]

[Borrower Name and Address]

Mortgage Statement

Statement Date: _______

Account Number |

____________ |

Payment Due Date |

____________ |

Amount Due |

____________ |

If payment is received after [DATE], $____ late fee will be charged.

Account Information

Outstanding Principal |

$_______ |

Interest Rate (Until [Date]) |

______% |

Prepayment Penalty |

[Yes/No] |

Explanation of Amount Due

Principal |

$_______ |

Interest |

$_______ |

Escrow (for Taxes and Insurance) |

$_______ |

Regular Monthly Payment |

$_______ |

Total Fees Charged |

$_______ |

Total Amount Due |

$_______ |

Transaction Activity (_/_/_ [Date] to _/_/_ [Date])

Date |

Description |

Charges |

Payments |

[Date] |

Late Fee (charged because full payment not received by _/_/_ |

$ |

|

[Date] |

Payment Received – Thank you |

|

$ |

[Date] |

Fee Description |

$ |

|

Past Payments Breakdown

|

Paid |

Paid |

|

Last |

Year to |

|

Month |

Date |

Principal |

$ |

$ |

Interest |

$ |

$ |

Escrow (Taxes and Insurance) |

$ |

$ |

Fees |

$ |

$ |

Total |

$ |

$ |

[Servicer Name and Address]

Amount Due

Due By _/_/_ [Date]$

$___ late fee will be charged after [Date]

Additional Principal |

$ |

Additional Escrow |

$ |

Total Amount Enclosed |

$ |

Make check payable to [Servicer Name]

[Account Number]

[Additional tables to be translated]

Important Messages

*Partial Payments: Any partial payments that you make are not applied to your mortgage, but instead are held in a separate suspense account. If you pay the balance of a partial payment, the funds will then be applied to your mortgage.

**Delinquency Notice**

You are late on your mortgage payments. Failure to bring your loan current may result in fees and foreclosure – the loss of your home. As of [Date], you are __ days delinquent on your mortgage loan.

Recent Account History

·Payment due [Date]: Fully paid on time

·Payment due [Date]: Fully paid on [Date]

·Payment due [Date]: Unpaid balance of $________

·Current payment due [Date]: $_______

·Total: $_______ due. You must pay this amount to bring your loan current.

If you are Experiencing Financial Difficulty: See back for information about mortgage counseling or assistance.

Completing the Mortgage Statement form accurately is essential for managing your mortgage effectively. Following these steps will help ensure that you fill out the form correctly, allowing you to stay informed about your mortgage account and any associated fees.

Misconceptions about the Mortgage Statement form can lead to confusion and financial missteps. Here are four common misunderstandings:

Understanding these misconceptions can help you manage your mortgage more effectively and avoid potential pitfalls.

When managing a mortgage, various forms and documents are essential to ensure clarity and compliance. Each document serves a specific purpose in the mortgage process, providing both the borrower and lender with critical information regarding the loan. Below are some commonly used documents alongside the Mortgage Statement form.

Understanding these documents can help borrowers navigate their mortgage responsibilities more effectively. Each plays a vital role in ensuring that both the borrower and lender are informed and protected throughout the life of the loan.