Free Personal Guarantee Form

Free Personal Guarantee Form

Private Mortgage Contract - Buyers often have the ability to negotiate purchase price and terms directly with the seller.

In addition to the essentials of the Colorado Real Estate Purchase Agreement form, it is important for buyers and sellers to familiarize themselves with the resources available for completing this process effectively. For those looking for a reliable template, the Colorado PDF Forms website offers a convenient printable version that can help streamline the agreement process.

Purchase Agreement Addendum - Use this form to add specific conditions to a purchase agreement.

Termination Agreement Real Estate - This form can also specify who pays for any associated costs, if necessary.

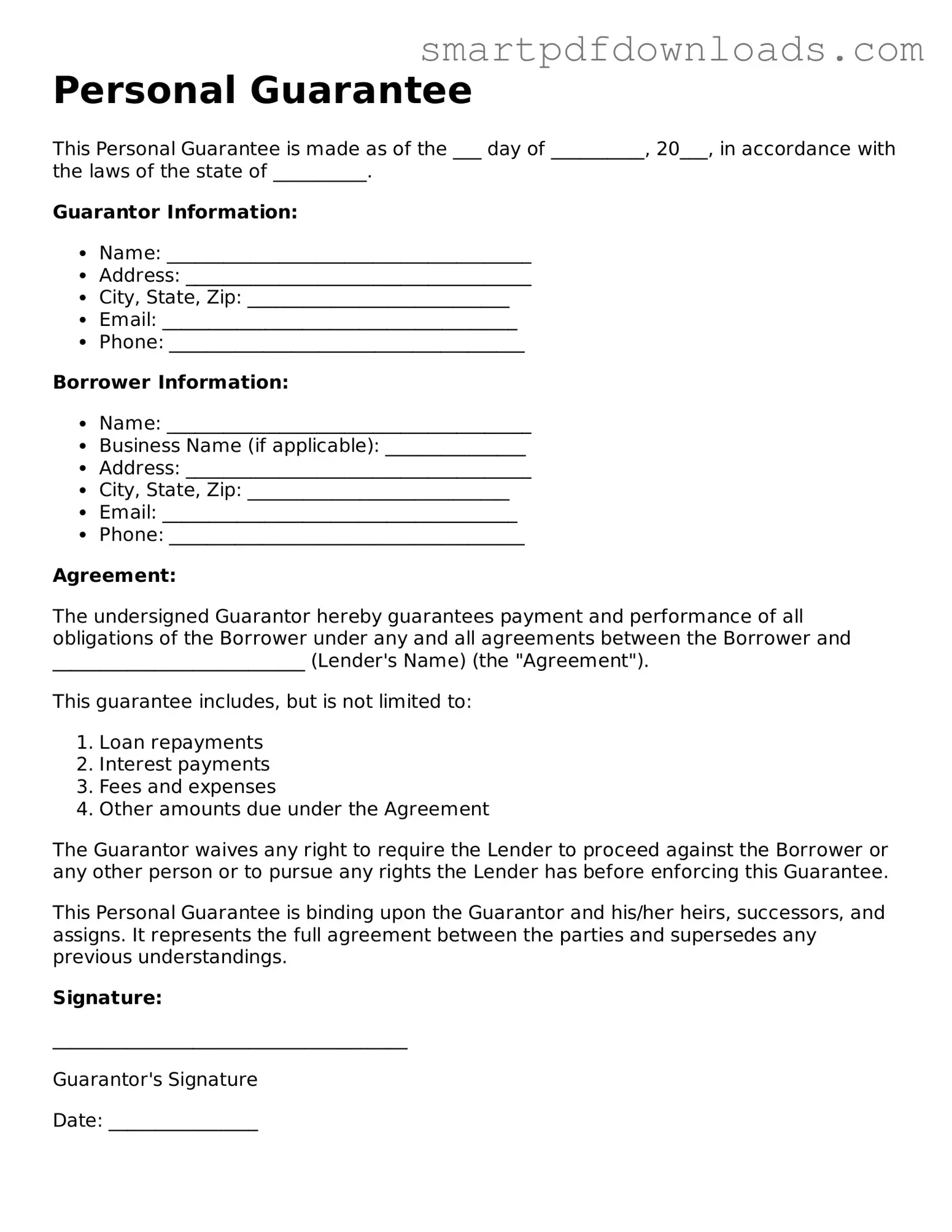

Personal Guarantee

This Personal Guarantee is made as of the ___ day of __________, 20___, in accordance with the laws of the state of __________.

Guarantor Information:

Borrower Information:

Agreement:

The undersigned Guarantor hereby guarantees payment and performance of all obligations of the Borrower under any and all agreements between the Borrower and ___________________________ (Lender's Name) (the "Agreement").

This guarantee includes, but is not limited to:

The Guarantor waives any right to require the Lender to proceed against the Borrower or any other person or to pursue any rights the Lender has before enforcing this Guarantee.

This Personal Guarantee is binding upon the Guarantor and his/her heirs, successors, and assigns. It represents the full agreement between the parties and supersedes any previous understandings.

Signature:

______________________________________

Guarantor's Signature

Date: ________________

By signing, the Guarantor acknowledges that he/she has read and understands this Personal Guarantee.

Completing the Personal Guarantee form is an important step in securing a commitment. After filling out the form, it will be submitted to the relevant parties for review. Ensure that all information is accurate and complete to facilitate a smooth process.

The Personal Guarantee form is often misunderstood, leading to confusion among individuals and businesses. Here are nine common misconceptions about this important document, along with clarifications to help demystify it.

Understanding these misconceptions can help individuals and businesses navigate the complexities of personal guarantees more effectively. Being informed is crucial when entering into any financial agreement.

A Personal Guarantee form is often used in various business and financial transactions to provide assurance that an individual will fulfill a financial obligation. However, several other documents may accompany this form to ensure clarity and protect the interests of all parties involved. Below is a list of these documents, each serving a specific purpose in the overall agreement.

Understanding these documents and their roles can greatly enhance the clarity and security of financial transactions. Each plays a vital part in ensuring that all parties are protected and informed throughout the process.