Profit And Loss Form

Profit And Loss Form

Free Broker Price Opinion Template - The last sale provides a historical context for market fluctuations.

This essential guide to the Residential Lease Agreement highlights the key elements to consider when entering into a rental agreement. It is crucial for both landlords and tenants to be familiar with the terms outlined in the document to ensure a mutually beneficial partnership. For further details, you can refer to the Ohio Residential Lease Agreement template.

Dollar Sheet Fundraiser - Your dollar donation goes a long way.

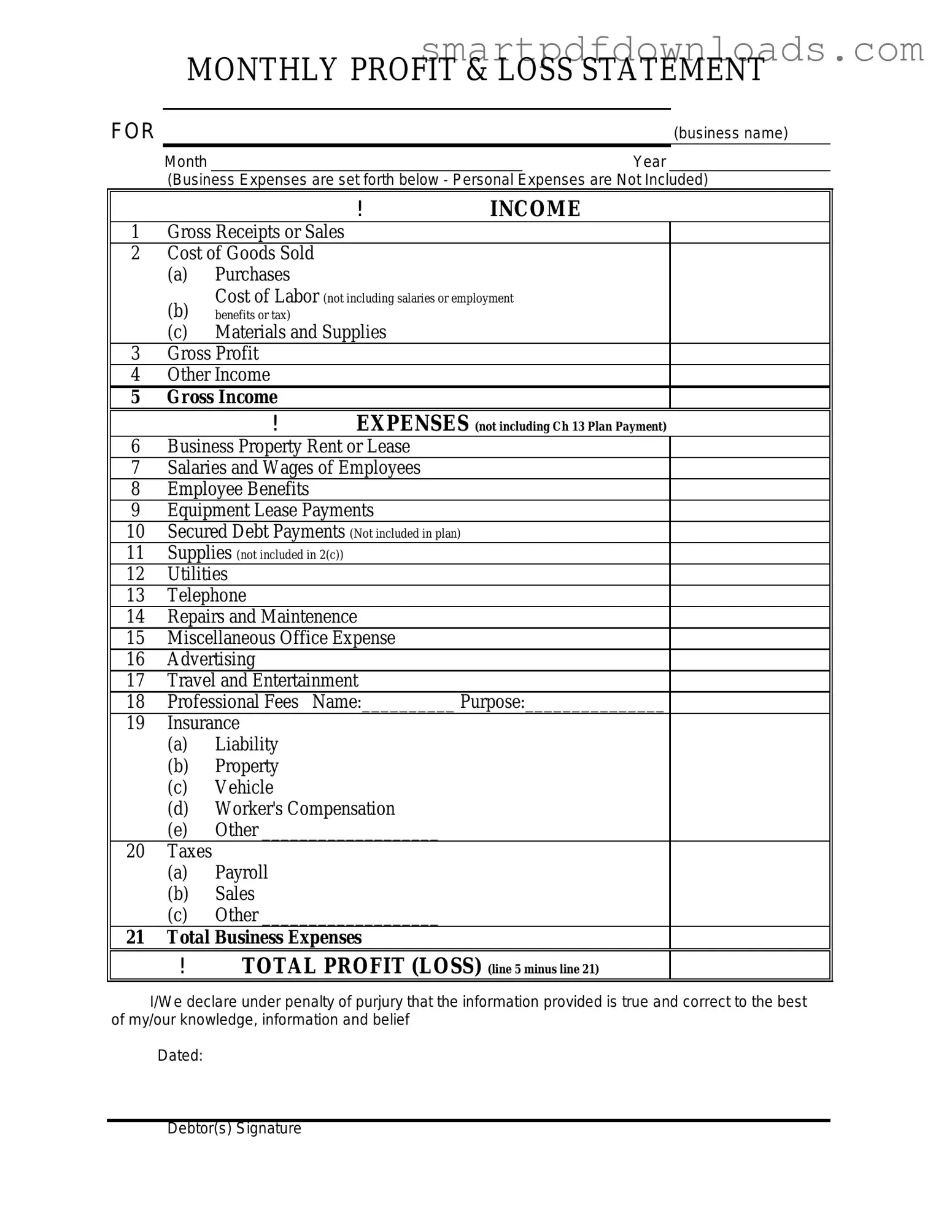

MONTHLY PROFIT & LOSS STATEMENT

FOR |

(business name) |

Month |

Year |

(Business Expenses are set forth below - Personal Expenses are Not Included)

|

|

|

! |

INCOME |

1 |

Gross Receipts or Sales |

|

||

2 |

Cost of Goods Sold |

|

||

|

(a) |

Purchases |

|

|

|

(b) |

Cost of Labor (not including salaries or employment |

||

|

benefits or tax) |

|

|

|

|

(c) |

Materials and Supplies |

|

|

3 |

Gross Profit |

|

|

|

4 |

Other Income |

|

|

|

5 |

Gross Income |

EXPENSES (not including Ch 13 Plan Payment) |

||

|

|

! |

||

6 |

Business Property Rent or Lease |

|

||

7 |

Salaries and Wages of Employees |

|

||

8 |

Employee Benefits |

|

|

|

9 |

Equipment Lease Payments |

|

||

10 |

Secured Debt Payments (Not included in plan) |

|

||

11 |

Supplies (not included in 2(c)) |

|

||

12 |

Utilities |

|

|

|

13 |

Telephone |

|

|

|

14 |

Repairs and Maintenence |

|

||

15 |

Miscellaneous Office Expense |

|

||

16 |

Advertising |

|

|

|

17 |

Travel and Entertainment |

|

||

18 |

Professional Fees |

Name:__________ Purpose:_______________ |

||

19 |

Insurance |

|

|

|

|

(a) |

Liability |

|

|

|

(b) |

Property |

|

|

|

(c) |

Vehicle |

|

|

|

(d) |

Worker's Compensation |

|

|

|

(e) |

Other ___________________ |

|

|

20 |

Taxes |

|

|

|

|

(a) |

Payroll |

|

|

|

(b) |

Sales |

|

|

|

(c) |

Other ___________________ |

|

|

21 |

Total Business Expenses |

|

||

|

! |

TOTAL PROFIT (LOSS) (line 5 minus line 21) |

||

I/We declare under penalty of purjury that the information provided is true and correct to the best of my/our knowledge, information and belief

Dated:

Debtor(s) Signature

Completing the Profit and Loss form is an essential step in tracking your financial performance. It helps you understand your income and expenses over a specific period, allowing you to make informed decisions for your business. Follow these steps to fill out the form accurately.

The Profit and Loss (P&L) form, often referred to as the income statement, serves as a crucial financial document for businesses. However, several misconceptions surround its purpose and usage. Here are eight common misunderstandings:

Understanding these misconceptions can help individuals and businesses better utilize the Profit and Loss form as a tool for financial management and strategy.

The Profit and Loss form is a vital tool for businesses to assess their financial performance over a specific period. However, it often works in conjunction with several other important documents. These forms help provide a comprehensive view of a company's financial health and assist in making informed decisions. Here’s a list of documents commonly used alongside the Profit and Loss form:

Understanding these forms and how they interact with the Profit and Loss form is crucial for any business. Each document plays a unique role in painting a complete picture of financial performance, guiding strategic decisions, and ensuring long-term success.